The Most Common Multi-scheme Fraud Cases

/ GUEST BLOGGER

GUEST BLOGGER

John Warren, J.D., CFE

ACFE Vice President and General Counsel

Readers of the ACFE’s 2012 Report to the Nations are probably familiar with the statistics we compile on the frequency and cost of the 11 most common occupational fraud schemes: financial statement fraud, corruption, billing schemes, expense reimbursements, check tampering, payroll fraud, cash register disbursements, skimming, cash larceny, theft of cash on hand and non-cash misappropriations. But one thing that probably does not receive enough attention in our study is how fraudsters tend to commit multiple forms of fraud within a single case. For instance, an employee who is committing a billing scheme may also be involved in payroll fraud, check tampering, corruption or some other form of misconduct.

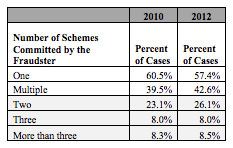

We looked at the data from our last two Reports to see how often fraudsters engaged in multi-scheme crimes, and we found that the results were very similar for the two data sets. In 2010, 40 percent of frauds involved multiple schemes, while in 2012 the number was 43 percent. Furthermore, the distribution of cases involving two schemes, three schemes or more than three schemes was remarkably consistent.

Based on the data shown above, it appears that we can expect around 40-43 percent of occupational frauds to involve multiple schemes. If that is the case, then how can we make use of this information to improve our ability to detect multi-scheme frauds? The first thing we would like to know is whether certain types of schemes tend to be associated with one another. For instance, if we know that people who commit payroll fraud are likely to also commit billing fraud but not as likely to engage in the theft of non-cash assets, then that can help us focus our examinations on the most likely areas of risk.

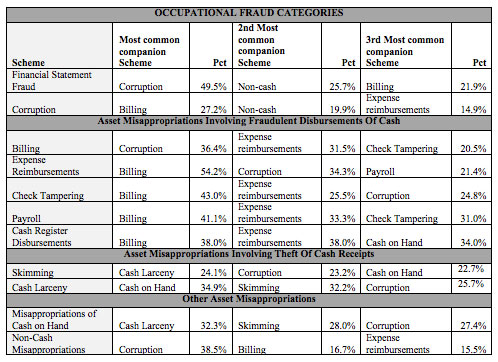

In the table below we have presented the three most common companion schemes for each of the 11 occupational fraud categories. (This data is based on cases from our 2012 study). For example, in the first row we can see that 49.5 percent of fraudsters who committed financial statement fraud were also involved in some form of corruption; 25.7 percent were misappropriating non-cash assets; and 21.9 percent were involved in a billing scheme.

The bottom line is, whenever you uncover fraud committed by an employee, manager or executive, there is a very good chance that the fraudster’s misconduct extends beyond the first scheme you identify. CFEs should keep the data shown here in mind during their examinations and run appropriate tests and reviews to identify all forms of fraud that a perpetrator may be committing.