GUEST BLOGGER

Sarah Hofmann

ACFE Public Relations Specialist

“Waste, fraud and abuse” has become a pervasive soundbite in the 2016 U.S. presidential election, but just how much fraud is actually occurring in the government? In a study of 2,410 occupational fraud cases investigated by Certified Fraud Examiners (CFEs) between January 2014 and October 2015, 18.7 percent of the reported fraud instances occurred in government entities. Although the instances of reported fraud in the government occurred at an equal frequency between local, state and federal government, cases that occurred on the federal level cost a median of $194,000 each — a noticeably higher level than the median cost of fraud at the local and state government levels ($80,000 and $100,000 respectively).

The Association of Certified Fraud Examiners (ACFE) published the results of its most recent global fraud survey in its highly anticipated 2016 Report to the Nations on Occupational Fraud and Abuse. Other key findings from the 92-page report include (all values in U.S. dollars):

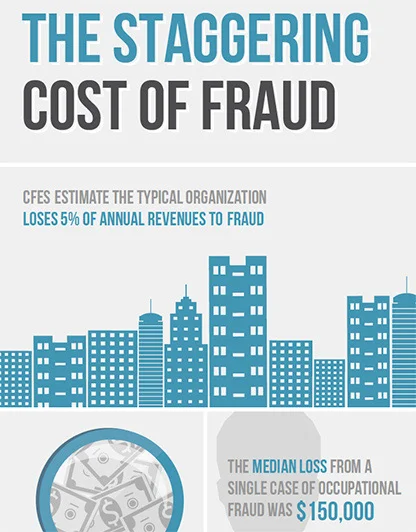

Fraud is incredibly costly. The total cost of the frauds reported in the study was over $6.3 billion, with 23 percent of the cases costing more than $1 million. The study respondents estimated that the typical organization loses 5 percent of its annual revenue to fraud each year. When applied to the 2014 estimated Gross World Product of $74.16 trillion, this translates to potential global fraud losses of up to $3.7 trillion.

Small businesses are especially at risk. The study found that organizations with fewer than 100 employees faced the same median cost per instance of fraud as companies with more employees. However, less than half of the smaller organizations had implemented some of the most basic anti-fraud controls like implementing a fraud hotline, and establishing a management review and code of conduct.

Hotlines are becoming an expected control in most companies. In the study, CFEs reported that 60.1 percent of the organizations they worked with had a fraud reporting hotline in place, an 8.9 percent increase from the findings reported in 2010.

Physical documents are still key components in fraud. For the first time, respondents were asked how fraudsters attempted to cover their tracks. Even in such a technologically driven world, fraudsters are still relying on creating fraudulent physical documents, altering existing physical documents or destroying those documents.

The Report to the Nations also details findings such as how fraud risks varied by industry, how the implementation of anti-fraud controls affected exposure to fraud, the breakdown of fraud statistics by geographical region and the most common behavioral traits observed among fraud perpetrators.

The 2016 Report to the Nations is available for download online at ACFE.com/RTTN.