4 Ways to Protect Your Company’s Pot of Gold

/

AUTHOR'S POST

Mandy Moody, CFE

ACFE Content Manager

Don’t worry; I’m not going to go all Lucky Charms on you this St. Patrick’s Day and toss out a bunch of thinly veiled Irish puns. You would only be so lucky…sorry, I couldn’t resist.

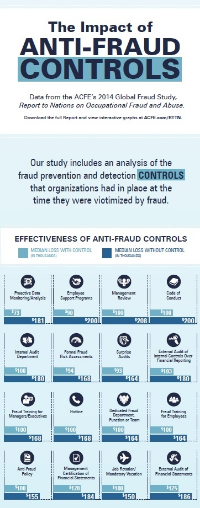

But, I did want to take this opportunity to remind you about the cost of fraud to your organization and how to add four easy best practices that will help protect your company’s hard-earned pot of gold. Organizations worldwide lose an estimated 5 percent of their annual revenues to fraud, according to the ACFE’s 2016 Report to the Nations on Occupational Fraud and Abuse. A single instance of fraud can be devastating: the median loss per fraud case was $145,000, and more than a fifth of the cases involved losses of at least $1 million.

The good news? There are some basic steps your organization can take to lessen your vulnerability to fraud:

1. Adopt a Code of Ethics.

Be proactive in setting a tone for management and employees. Evaluate your internal controls for effectiveness and identify areas of the business that are vulnerable to fraud.

2. Establish Hiring Procedures.

When hiring staff, conduct thorough background investigations. Check educational, credit and employment history (as permitted by law), as well as references.

3. Implement a Fraud Hotline.

Fraud is still most likely to be detected by a tip. Providing an anonymous reporting system for your employees, contractors and clients will help uncover more fraud.

4. Increase the Perception of Detection.

Communicate regularly to staff about anti-fraud policies, ways to report suspicions of misconduct, and the potential consequences (including termination and prosecution) of fraudulent behavior.

Implementing these tips could help prevent your organization from becoming a statistic, and help keep your pot of gold safe and secure. I leave you with this Irish blessing: “Here’s to you and yours, And to mine and ours, And if mine and ours ever come across you and yours, I hope you and yours will do as much for mine and ours as mine and ours have done for you and yours!” Cheers, everyone!