Report to the Nations: The Top 5 Ways Fraud Affects Your Bottom Line

/

AUTHOR'S POST

Mandy Moody, CFE

ACFE Media Manager

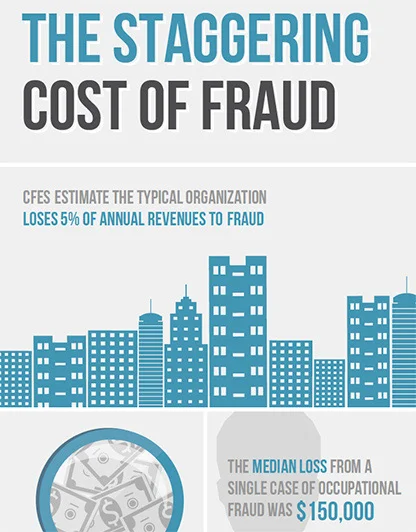

The ACFE's 2016 Report to the Nations on Occupational Fraud and Abuse provides an analysis of 2,410 cases of occupational fraud that occurred in 114 countries throughout the world. What makes this analysis so valuable is its ability to give readers a true idea of the toll fraud can take on a company.

Here are the top five conclusions that describe the impact fraud can have on the bottom line:

- Asset misappropriation was by far the most common form of occupational fraud, occurring in more than 83% of cases, but causing the smallest median loss of $125,000. Financial statement fraud was on the other end of the spectrum, occurring in less than 10% of cases but causing a median loss of $975,000. Corruption cases fell in the middle, with 35.4% of cases and a median loss of $200,000.

- The longer a fraud lasted, the greater the financial damage it caused. While the median duration of the frauds in our study was 18 months, the losses rose as the duration increased. At the extreme end, those schemes that lasted more than five years caused a median loss of $850,000.

- Approximately two-thirds of the cases reported to us targeted privately held or publicly owned companies. These for-profit organizations suffered the largest median losses among the types of organizations analyzed, at $180,000 and $178,000, respectively.

- Of the cases involving a government victim, those that occurred at the federal level reported the highest median loss ($194,000), compared to state or provincial ($100,000) and local entities ($80,000).

- Although mining and wholesale trade had the fewest cases of any industry in our study, those industries reported the greatest median losses of $500,000 and $450,000, respectively.\

It is impossible to know exactly how much fraud goes undetected or unreported, and even calculations based solely on known fraud cases are likely to be underestimated, as many victims downplay or miscalculate the amount of damage. Nonetheless, attempts to determine the cost of fraud are important, because understanding the size of the problem helps bring attention to its impact, enables organizations to quantify their fraud risk, and helps management make educated decisions about investing in anti-fraud resources and programs.

Find more takeaways and download the full report at ACFE.com/RTTN.