Report Highlights Top Fraud Trends in the Asia-Pacific Region

/GUEST BLOGGER

Andi McNeal, CFE, CPA

ACFE Research Director

In 2010, the ACFE released the results of our first ever global fraud survey; all of our previous research had been limited to fraud cases in the U.S. The results of our international research revealed that the characteristics of fraud cases and perpetrators follow some universal patterns, but that each geographical region faces unique challenges. Our second global study in 2012 reinforced this observation.

With this in mind and in light of the upcoming 2012 ACFE Asia-Pacific Fraud Conference, we thought it would be interesting to look more closely at some of the trends in the 176 fraud cases from our 2012 study that were reported from the Asia-Pacific region. (For purposes of this analysis, we included the cases from the following countries: Australia, China, Fiji, India, Indonesia, Japan, Malaysia, New Zealand, Philippines, Singapore, South Korea, Taiwan, Thailand, and Vietnam. This breakdown differs from the “Asia” region as discussed in the full 2012 Report to the Nations on Occupational Fraud and Abuse.)

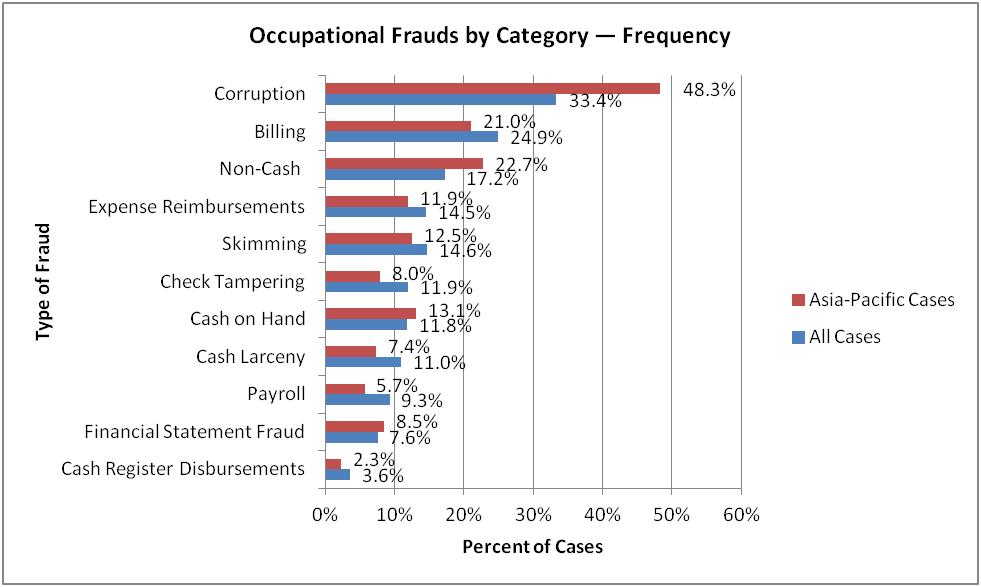

The following chart compares the methods used by fraudsters in Asia-Pacific countries to those employed by fraudsters throughout the world. We see that corruption schemes were significantly more common in the Asia-Pacific region, and misappropriation of non-cash assets also occurred more frequently in this region than was observed overall.

Among our most notable observations was that overall losses were higher in the Asia-Pacific region than for the full sample of cases in our 2012 study. The median loss for the 176 Asia-Pacific cases was US$235,000, compared to a median loss of US$140,000 for all cases. And the median loss was greater in eight of the 11 fraud scheme sub-categories we studied, with the biggest disparity in the losses related to financial statement frauds. The median loss for those cases in the Asia-Pacific region was US$4 million, or four times the median loss for all financial statement fraud cases studied.

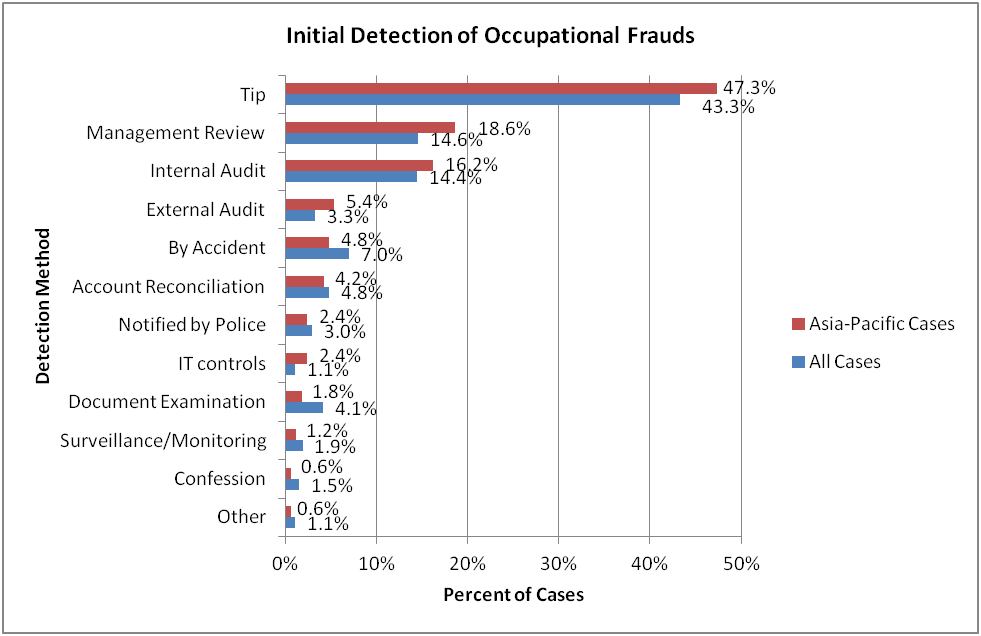

In examining how frauds in the Asia-Pacific region were detected, we found that the distribution of detection methods was very similar to that observed overall; that is, tips were by far the most common way frauds were detected, followed by management review and internal audit. Together these three mechanisms accounted for more than 80 percent of frauds detected in the Asia-Pacific region and approximately 72 percent of frauds detected throughout the world.

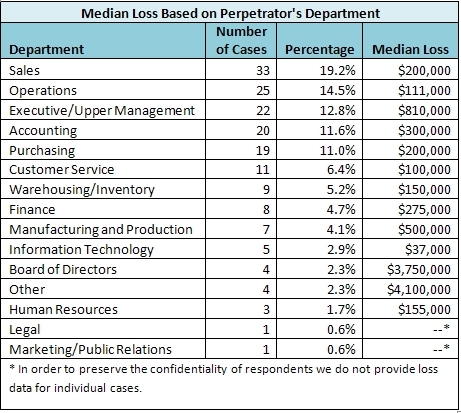

The table below shows the breakdown of the fraud cases in the Asia-Pacific region by the department in which the perpetrator worked and provides the median loss for the cases associated with each department. When we compared these findings to our overall study results, we noted that fraud was much more common in the Sales and Purchasing departments in the Asia-Pacific region, whereas fraud in the Accounting department occurred much less frequently in that region than in the full sample of cases.

As anti-fraud professionals in the Asia-Pacific region gather to learn and network, we hope this information helps them focus their efforts and assists them in working together in the fight against fraud.